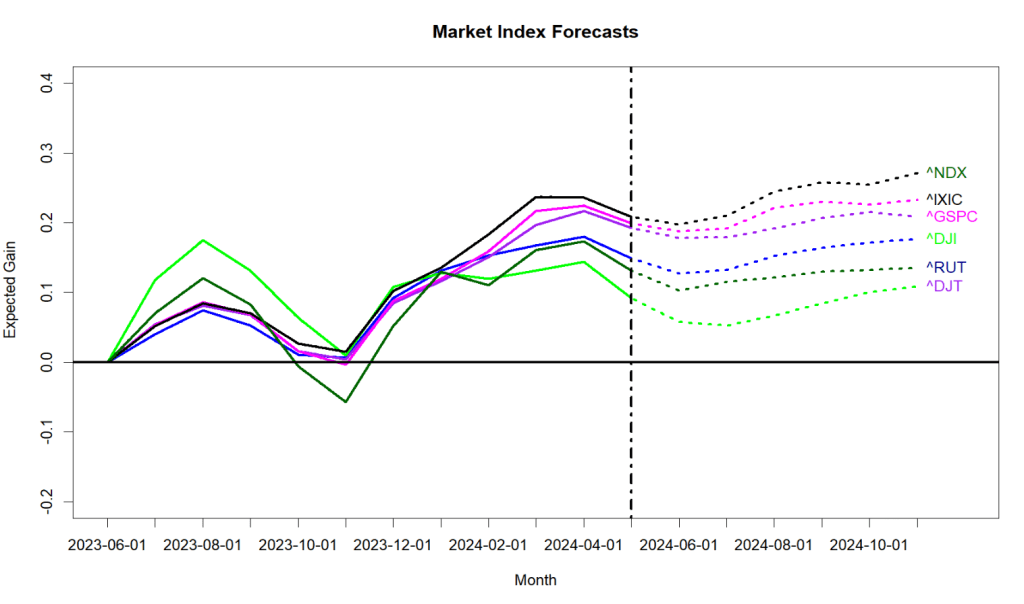

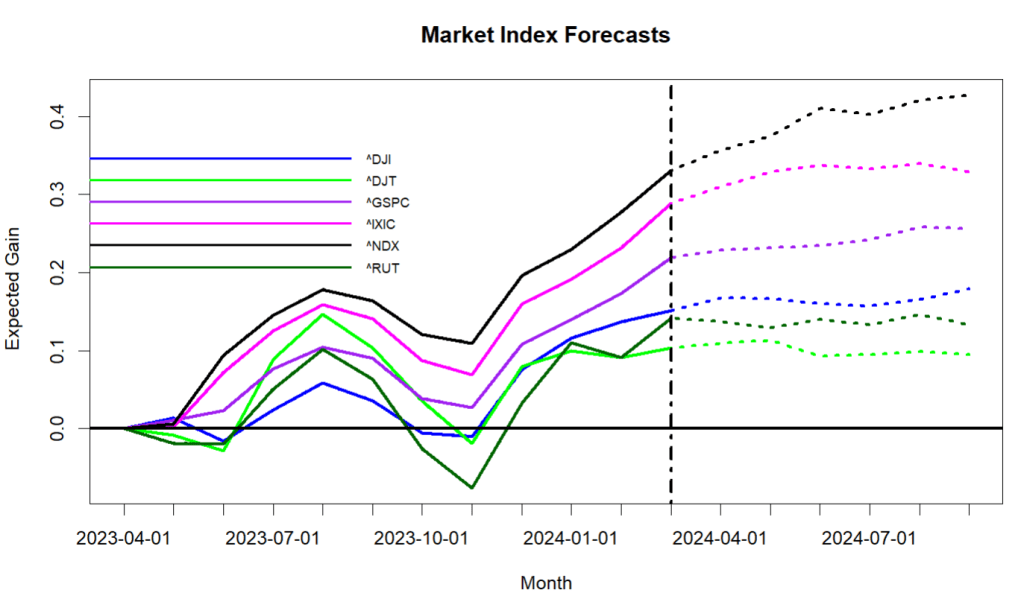

November forecast will come in a couple of days. This is just words.

If Republican election fraud claims have any credibility, the national network of Democratic election fraud collaborators must be astounding! Think of it, a vast conspiracy of operatives working in thousands of local government electoral precincts, but leaving no trace of their efforts. No emails. No letters. No witnesses willing to squeal for big chunks of money. But, especially, no telltale statistical evidence. Damn these guys are smart!

For context. In World War II the Allies managed to repeatedly break the German Enigma coding system. It is a fascinating story that is well worth the read. Suddenly, the Allies were able to instantly read all critical war communications – orders, troop movements, distribution plans, everything! But, they realized that if they took advantage of all of their intelligence, the Germans would realize that their code system had been compromised and would quickly change code systems thereby eliminating the Allied edge. So, consciously the Allies kept Enigma intelligence (Ultra) in a crucial but limited manner.

German statisticians would only be able to prove that the Allies were smart, maybe even lucky, but the Allies success was not much more than could be statistically random. There would be no statistical proof that the Allies results had surged unexpectedly. Allied moves would not betray the fact the code had been broken. Thousands of Allied soldiers died because their groups were not given critical code data that the Allies had gleaned. But, that was the price the Allies were willing to pay to keep their secret of having broken the Enigma code.

Back to today. The US election system is operated by the states and US territories. Within the states there are fixed rules for voter registration and voting. Voter registration occurs through state agencies, but actual voting occurs through hundreds or thousands of local precincts. Voting lists are public as are data on who voted in which elections. The only thing that is secret is how each voter actually voted. In nearly all precincts the voting data goes back for decades.

With all of this public voting data – going down to the level of which particular voter voted in which elections along with their party affiliation – it becomes a Statistics 101 class effort to identify voting irregularities. There is a laundry list of things to check first: Who died? Who moved, and are they voting twice? But, overall, the gross voting numbers would indicate if the results in any of thousands of voting places was unusual. Audits like this are routine in all states after each election.

In the modern era with voting data being public it probably still would not be too difficult to twist the voting outcome a bit in any single precinct.

But, today it would be an incredible effort for a group to significantly shift just a single state-level election. It would take hundreds of people and control of highly secured voting machines, all working in total secrecy for years at a time. But, for a political party to run such an effort in at least all the swing states would be an absolutely breathtaking effort.

If they are doing it, DAMN THOSE GUYS ARE GOOD!

d