We have little modern economic precedent for a 50% spike in oil prices with further room to run. The only true parallels are the embargoes of 1973 and 1979. While a barrel of crude sat at $60 last fall, it commands $99 today. As the world’s largest producer, the U.S. is better shielded from physical shortages than most countries, yet domestic prices have instantly aligned with soaring global markets. We won’t see major oil shortages, but we may experience shortages of other goods that pass the Strait of Hormuz such as fertilizer. Regardless, almost certainly we will have a spike in inflation.

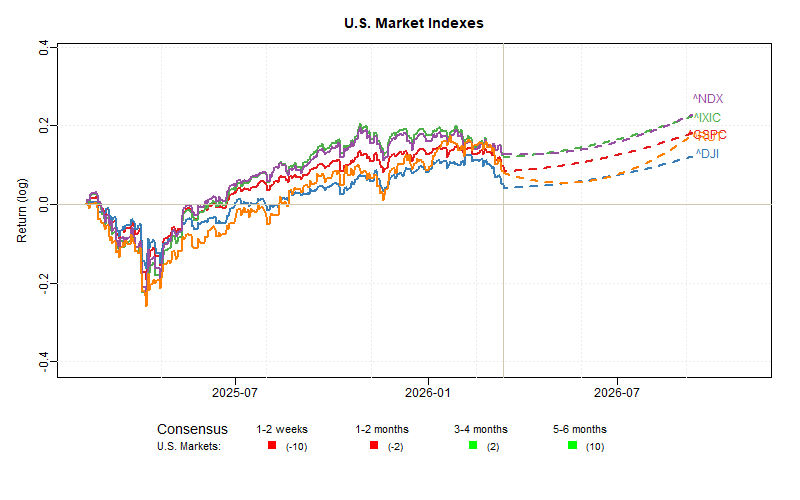

My short-term market forecasts have turned sharply negative. While 3-to-6-month models suggest a rebound, I am viewing that optimism with skepticism; these models weren’t trained on the structural “scars” left by the 1970s crises. With rising unemployment, stubborn inflation, and tepid GDP growth, the market is currently fueled by bad news. If oil doesn’t stabilize soon, the situation could degrade rapidly.