The forecasting model says:

July: -0.3% (below average, typical for summer)

Next 6 Montlhs: 4% (slightly below average)

Probability of at least breaking even: 0.59 to 0.96 (Above average)

What am I doing? Staying fully invested. Expecting continued volatility through the November mid-term congressional elections.

Spoiler Alert: Eventually the stock market will crash — before the business cycle turns sour — and most probably as a direct result of the Federal Reserve relentlessly raising interest rates to rein in a frothy economy. But, don’t hold your breath waiting for the crash. At least, not for a year or more.

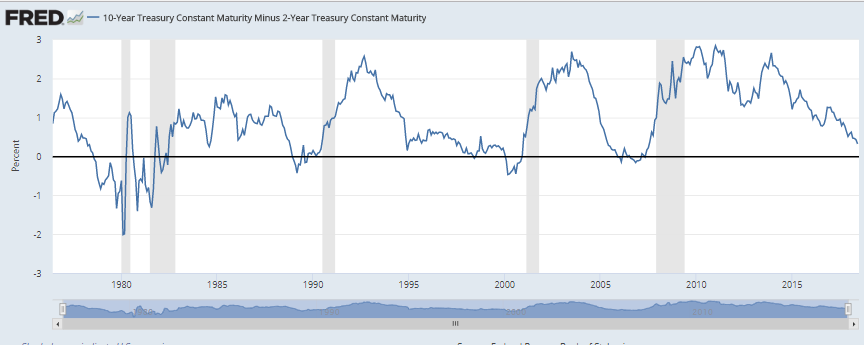

The difference between short and long term interest rates, the so-called “interest rate spread” shows in very slow motion how the Fed can, and will, choke off the economy when it decides to.

The nature of commercial lending is to borrow money on a short term basis at low rates and then lend it for long term projects at higher rates. The lender profits from the spread between the short and long term rates. (Think of a bank using your savings to make housing and car loans while paying you almost nothing in interest.) When short term interest rates start to equal, or even exceed, long term rates, the lending market dries up. Loans stop being made and the economy stumbles.

The Federal Reserve database chart above shows the half-century history of the spread between the 10-year Treasury bond interest rate and relatively short term 2-year interest rate. Over and over again, roughly a year after the short term rate equals of exceeds the long term rate the economy goes into recession. Routinely, the stock market crashes before the recession actually occurs.

The key take-away here is that the interest rate spread has been falling for several years and already is getting pretty low. It is almost time to start paying attention. A stock market crash now is on the visible horizon.

I remain convinced, however, that the next crash is still only on the far horizon — still one to three years away.